Determine monthly payments, total interest, and amortization details for various loans, enabling precise financial planning and comparison.

Calculation Results

Loan Amount:

Payment Amount:

Total Payments:

Total Interest:

Amortization Schedule

Period

Payment

Principal

Interest

Balance

Consider exploring complementary financial tools such as the Mortgage Calculator for home financing or the Auto Loan Calculator for vehicle purchase planning.

How the Loan Calculator Works

This comprehensive loan calculator evaluates general loan structures by computing the net loan amount and applying amortization principles to determine periodic payments. Enter the loan amount, annual interest rate, term in months, optional extra payments, payment frequency (monthly or bi-weekly), and start date. The tool calculates the payment amount, total payments, total interest, and a detailed schedule showing principal and interest allocation per period. An interactive line chart visualizes balance reduction and cumulative interest over time. For bi-weekly payments, the term is adjusted accordingly (e.g., 26 payments per year). Assumptions include fixed rates without prepayment penalties, focusing on core loan dynamics for planning.

Mathematical Formulas and Derivations

The periodic payment is derived from the annuity formula for fixed-rate loans:

\[ M = P \times \frac{r (1 + r)^n}{(1 + r)^n - 1} \]

Where \( M \) is the periodic payment, \( P \) is the loan principal, \( r \) is the periodic interest rate (annual / 12 for monthly, annual / 26 for bi-weekly), and \( n \) is the number of periods. For amortization, periodic interest is \( I = B \times r \), principal paid is \( Pr = M - I + extra \), and balance updates as \( B = B - Pr \). Total interest sums all \( I \), providing cost insights. Extra payments accelerate payoff, reducing interest.

Factors Influencing Loans and Their Costs

Credit and Security Dynamics

Loan rates are shaped by credit scores, collateral, and market conditions. Secured loans (e.g., with assets) offer lower rates due to reduced risk, while unsecured ones carry higher rates. Strong credit lowers costs; poor credit increases them.

Term, Frequency, and Adjustments

Longer terms reduce payments but boost interest; bi-weekly payments (26/year) shorten terms and save interest compared to monthly. Extra payments directly cut principal, minimizing compounding. Understanding these aids in cost optimization.

Factor

Influence

Cost Effect

Credit Score

Rate determination

High score reduces interest

Loan Term

Payment spread

Longer term increases total interest

Extra Payments

Principal reduction

Lowers total interest and term

Payment Frequency

Compounding adjustment

Bi-weekly saves on interest

Historical Loan Rates and Global Comparisons

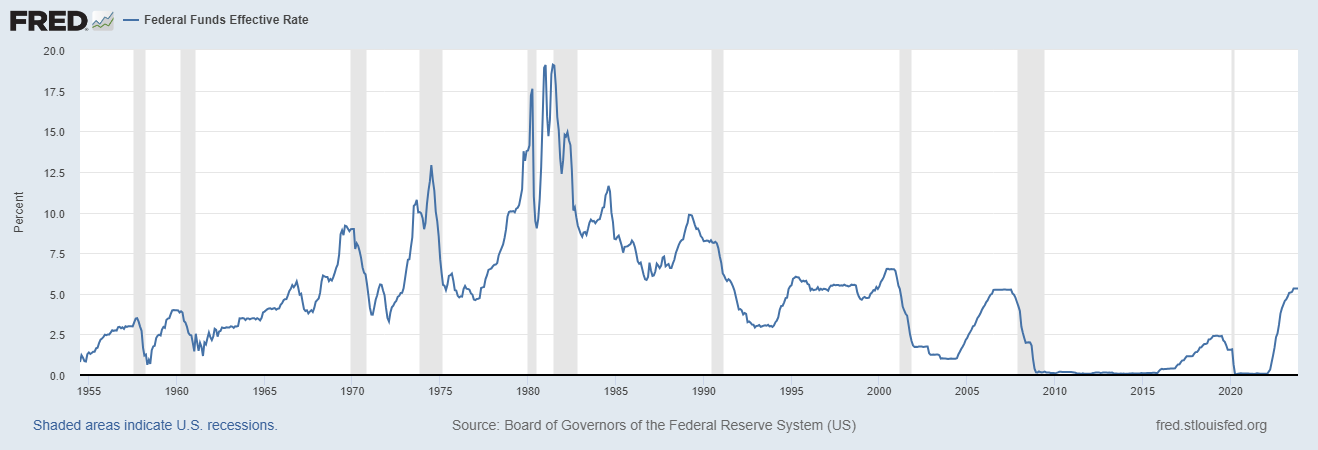

Loan interest rates have fluctuated with economic policies. In the U.S., Federal Reserve data indicates averages of 4-6% for consumer loans recently, with peaks over 8% in the 1980s due to inflation. Europe via ECB shows household loan rates at 3-7%, while World Bank data for emerging markets averages 6-10%. Rates dipped post-2008 but rose in 2022. The graph below depicts U.S. federal funds rate trends, influencing loan rates.

Historical chart of the effective Federal Funds Rate, influencing loan interest rates. Source: Wikipedia.

Global variations allow for better terms in stable economies. Use historical data for rate scenario modeling.

Region/Period

Average Rate (%)

Source

U.S. Recent

5.0

Federal Reserve

Europe (Households)

3.3-7.4

ECB

Emerging Markets

8.0

World Bank

1980s U.S. Peak

9.0

Federal Reserve

Historical loan contract from 1936, illustrating early loan practices. Source: Wikipedia.

Frequently Asked Questions

What factors affect payments? Principal, rate, term, frequency, and extras influence payments; higher rates or longer terms raise costs.

How do extra payments work? They reduce principal directly, shortening term and saving interest; input as monthly addition.

What's the difference in frequencies? Bi-weekly (every two weeks) results in 26 payments/year, paying off faster than monthly.

Why include start date? It dates the schedule for real-world planning, though calculations are period-based.

What if rates vary? Tool assumes fixed; rerun with averages for variables.

Disclaimer

This loan calculator is provided for educational and informational purposes only. It does not constitute financial, investment, or professional advice. Results are based on user inputs and assumptions; actual terms, rates, and costs may vary. Consult a qualified financial advisor or lender for personalized guidance. FCalculator.com assumes no liability for decisions made based on this tool.

This webpage offers an advanced loan calculator for projecting periodic payments, amortization schedules, and total costs, supporting monthly/bi-weekly frequencies, extra payments, start dates, interest rates, and terms. It features mathematical derivations, historical rate comparisons from Federal Reserve, ECB, and World Bank, interactive line charts for balance and interest trends, detailed tables, and PDF export. Suited for borrowers and planners, it focuses on affordability, optimization, and risk assessment, with disclaimers for professional advice.